Recently, China Everbright Bank released its 2025 Sustainable Development Report. The report aligns with the Shanghai Stock Exchange’s Guidelines for Sustainable Development Reporting by Listed Companies, the Hong Kong Stock Exchange’s ESG Reporting Guide, GRI Standards, and the SDGs. It has been subject to an independent limited assurance engagement by a third party. With a comprehensive framework, the report demonstrates a high level of disclosure compliance within the industry.

However, from a content perspective, the report provides relatively limited disclosure on risks and issues, exhibiting a pattern of “ample positive information and constrained negative information.” When cross-referenced with the bank’s recent regulatory performance and operational status, a certain tension emerges between its ESG disclosures and its actual risk profile.

Governance dimension: The report addresses corporate governance, risk management, and business ethics. China Everbright Bank has established a three-tier ESG governance structure (“decision-making layer – management layer – implementation layer”) and linked executive performance-based compensation to ESG performance. Additionally, in 2025, the bank conducted institutional audits of 13 directly affiliated branches or entities and carried out 40 special audits covering key areas such as green finance, risk classification, market risk, and operational risk. The governance system appears relatively robust at the policy level.

However, in contrast to the above institutional development, compliance issues at the implementation level remain prominent.

According to statistics, throughout 2025, the bank received over 40 regulatory fines (excluding individual penalties), with total penalties and forfeitures exceeding RMB 50 million. The violations spanned credit management, bill business, misreporting of regulatory data, internal control management, and even included the loss of a financial license. Entering 2026, the bank had already received more than 30 fines in the first quarter alone. For instance, the Jiaozuo branch was penalized multiple times within a short period for “violating regulations in handling foreign exchange settlement” and “inadequate post-loan management leading to the回流 of credit funds to borrowers; converting loans into deposits to inflate loan and deposit balances.”

The concentrated occurrence of diverse violations across multiple regions suggests that these are not isolated incidents at specific institutions but rather point to a systemic weakening of the internal control system at the implementation level.

At the same time, weaknesses have also surfaced in information disclosure management. In the bank’s 2025 annual report, data discrepancies appeared during the disclosure process on the two stock exchanges, involving asset size misstatements for 40 branch institutions. Notably, the bank initially performed a “silent replacement” of the SSE version without simultaneously issuing a correction announcement, only making a formal correction on the HKEX after public attention was drawn to the issue. This incident starkly contrasts with the report’s statement on “ensuring compliance and synchronization of information disclosure across the two markets,” revealing fragility in the bank’s internal control mechanisms for disclosure and posing a direct challenge to the rigor expected of a listed bank’s information disclosure.

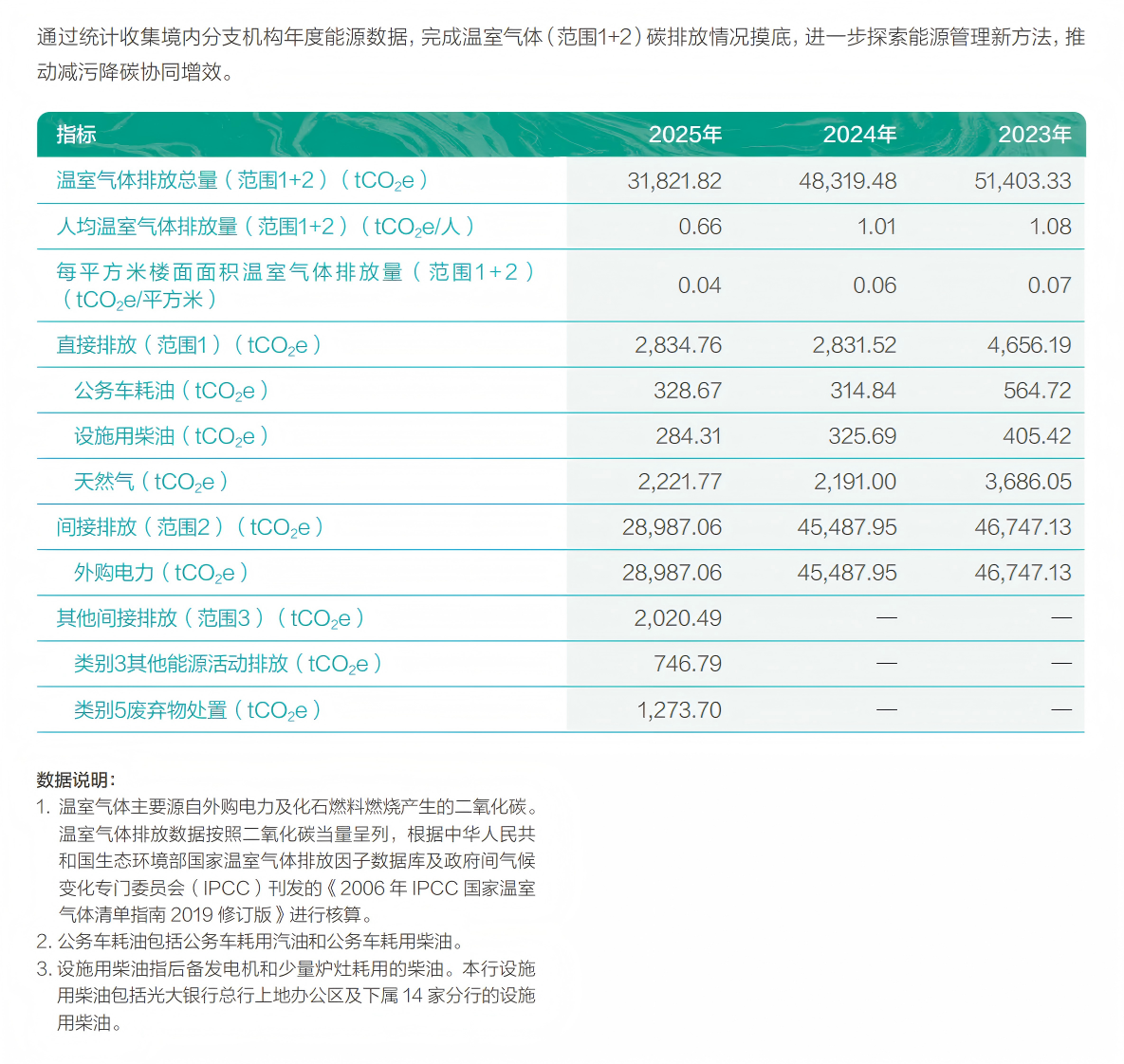

Environmental dimension: The report covers climate change response, green finance, and green operations. Data show that as of the end of 2025, China Everbright Bank’s green loan balance reached RMB 469.078 billion, a year-on-year increase of 13.57%, with its share of total loans rising to 11.68%. The bank also actively underwrote green bonds to support financing in clean energy, green building, and other sectors.

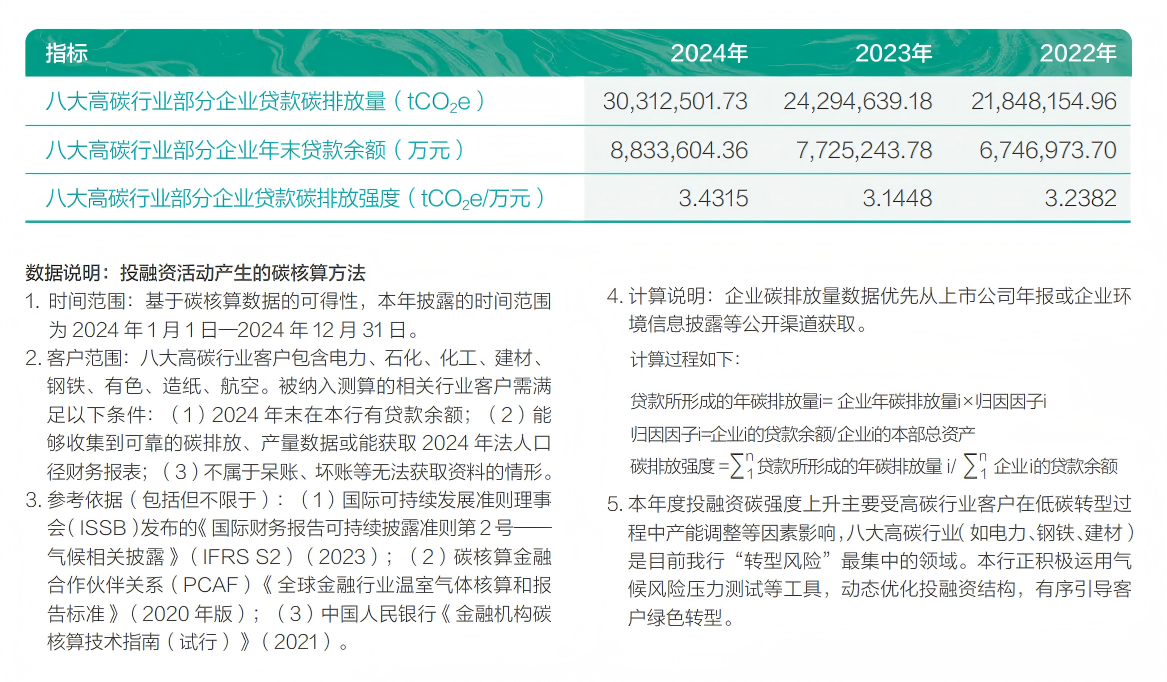

In terms of climate management, the bank has set a target to “peak its own operational carbon emissions by 2030,” identified climate-related physical risks, transition risks, and opportunities, disclosed Scope 1, 2, and 3 carbon emission data, and calculated the carbon footprint of some investment and financing activities for three consecutive years. In addition, the proportion of loans to eight high‑carbon industries declined compared to the previous year.

Nevertheless, in terms of disclosure depth, the above calculations remain largely focused on specific high‑carbon industry clients and have not yet extended to the broader credit asset portfolio. The boundary for Scope 3 carbon emission accounting is relatively limited, and a systematic methodological framework covering the entire asset portfolio has not yet been established.

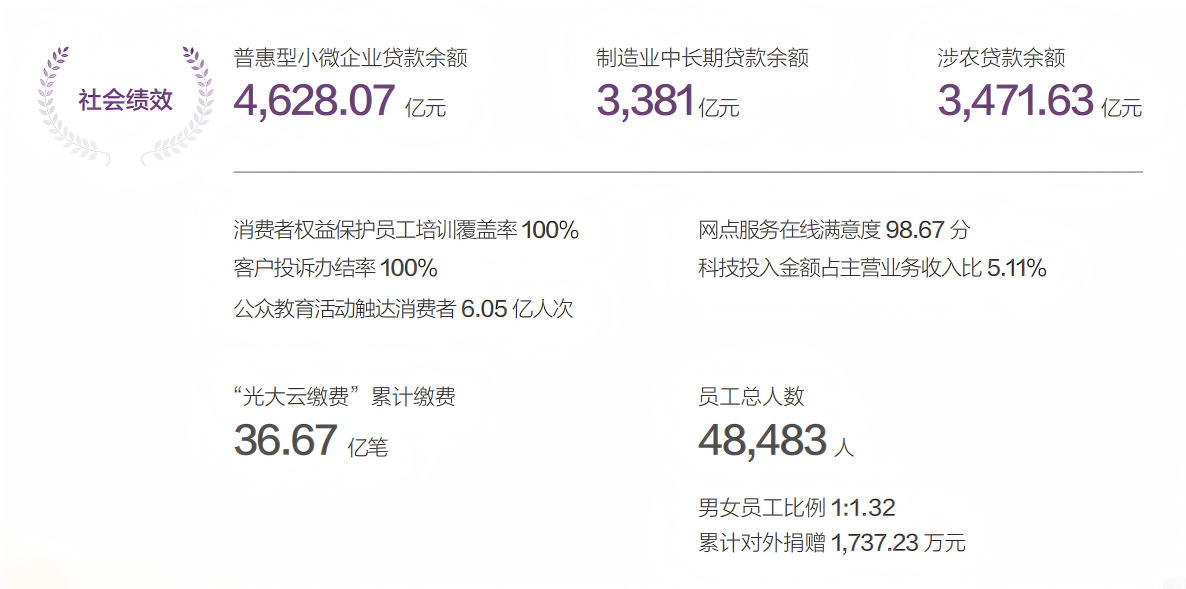

Social dimension: The report covers technology finance, inclusive finance, data security, customer privacy protection, and other areas, with relatively comprehensive information coverage.

Regarding consumer rights protection, the bank received 176,314 customer complaints in 2025, primarily concentrated in bankcard services (80.23%), debt collection (10.51%), and loan services (6.05%). The resolution rate for customer complaints was 100%, and the customer complaint satisfaction rate was 94.54%. However, the report does not provide a systematic analysis of the root causes of the high complaint volumes.

The Black Cat complaint platform shows that credit card business is a high‑incidence area for complaints, involving issues such as insufficient notification of annual fees, inadequate disclosure of installment costs, and revolving interest problems. These disputes point to concerns regarding product term transparency and service process standardization. The above issues indicate that the bank’s consumer protection management remains mainly focused on outcome‑based metrics, with insufficient attention to the causes of complaints and product‑design improvements, creating a certain gap relative to its consumer protection philosophy of “warm care, quality companionship.”

From an operational performance perspective: China Everbright Bank currently faces certain pressures: operating income has declined for four consecutive years; net profit fell nearly 7% year‑on‑year; net interest margin continues to narrow; and both non‑performing loan balance and ratio are on an upward trend, putting asset quality under strain.

Overall conclusion: China Everbright Bank’s 2025 Sustainable Development Report has achieved a relatively high level of compliance and structural completeness. However, the frequent recent regulatory penalties and information disclosure issues indicate a significant gap between the bank’s ESG commitments and its grassroots execution capabilities. For China Everbright Bank, how to genuinely embed ESG concepts into its internal control implementation and risk management system—rather than leaving them at the disclosure level—may become the key challenge it needs to address in its next stage of development.

Author:Qinger

Room 1808,Wayson Commercial Building, 28 Connaught Road West, Sheung Wan, Hong Kong.

Room 1808,Wayson Commercial Building, 28 Connaught Road West, Sheung Wan, Hong Kong.